Property vs Currency: Legal Classification Explained for Crypto Owners

Jun, 5 2026

Jun, 5 2026

Imagine you find a $100 bill in your pocket. You don't file paperwork to own it. You just spend it. Now imagine you buy a Bitcoin for $100. If its value jumps to $200, the government wants a cut of that profit before you can touch it. Why does the law treat these two forms of money so differently? The answer lies in a messy, centuries-old legal distinction between property and currency.

This isn't just academic trivia. It determines how much tax you pay, who gets your assets if you die, and whether you can sue someone who steals them. For years, the law treated cash as a universal medium of exchange and everything else-land, cars, stocks-as property. But with the rise of blockchain technology, that clear line has blurred into a gray zone that is causing headaches for lawyers, taxpayers, and regulators alike.

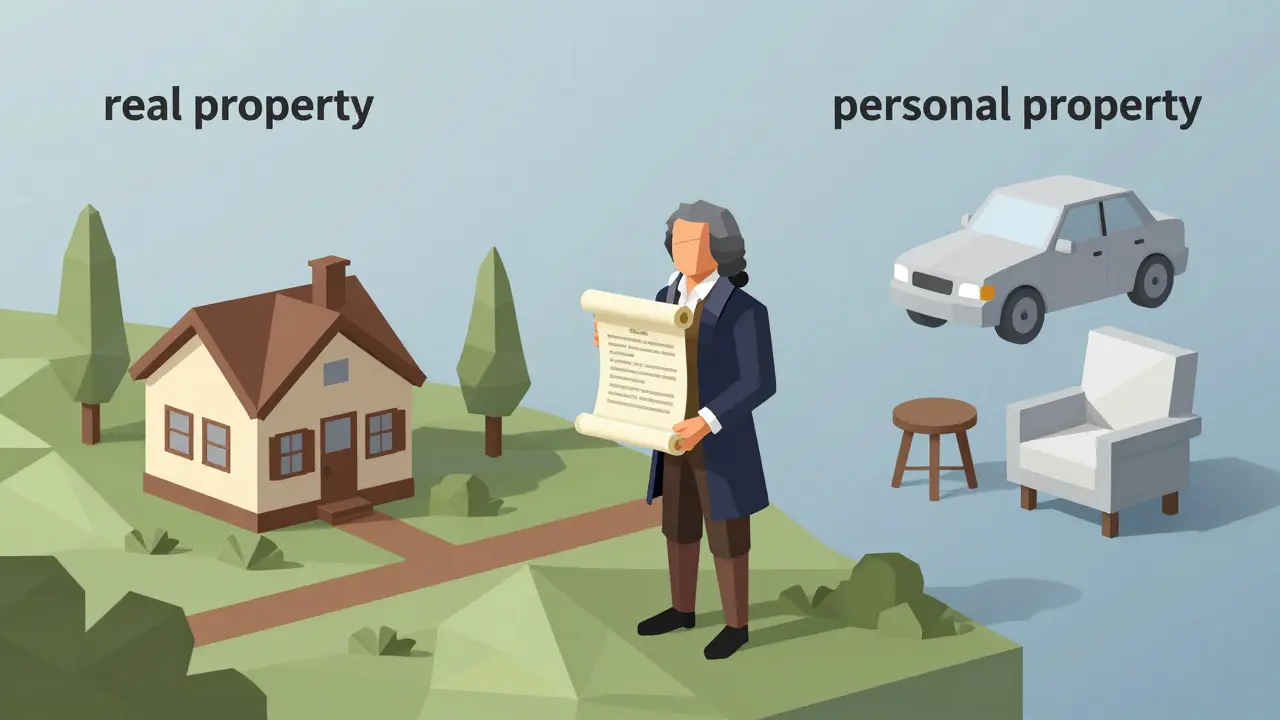

The Ancient Roots: Real vs. Personal Property

To understand where we are today, we have to look at where this system started. Modern property law traces its roots back to English common law, specifically William Blackstone’s Commentaries on the Laws of England from the late 1700s. Blackstone established a simple dichotomy: real property (land and things permanently attached to it) and personal property (movable items).

This distinction still drives the legal system. If you buy a house, you deal with deeds, county registries, and title insurance. This process costs money-often 0.5% to 1% of the property's value-and requires strict formalities. If you buy a couch, you just hand over cash and take it home. The law treats these transactions differently because land is unique and immovable, while furniture is replaceable.

The American Law Institute defines property not as the object itself, but as "the legal relationship between persons with respect to a thing." This means property rights are relational. They define what you can do against others. When you hold physical cash, those relationships change. Cash is technically classified as tangible personal property under the Federal Reserve Act, but courts often treat it differently because of its function as a medium of exchange.

Why Money Is Not Just Another Asset

You might think, "Cash is just an asset like my car or my laptop." Legally, it’s more complicated. In the landmark case Webb v. United States (1925), the Supreme Court established that money, when used in regular business, is not property but the "representative and measure of property."

Think about it. If someone steals your car, you sue for the specific car or its replacement value. If someone steals your cash, you sue for the amount lost. The law views cash as fungible-every dollar is identical to every other dollar. Your specific serial number doesn't matter. This fungibility allows money to flow through the economy without the friction of tracking individual ownership history for every transaction.

However, once that cash leaves your hand and enters a bank account, its legal nature shifts again. In United States v. Bajakajian (1998), the Supreme Court ruled that money in a bank account is a "chose in action"-a right to payment-rather than physical property. This is why your bank balance is intangible personal property. You don't own the paper bills; you own the debt the bank owes you.

The Crypto Conundrum: Property or Currency?

This brings us to the biggest legal headache of the 2020s: cryptocurrency. When Bitcoin emerged, no one knew how to classify it. Was it a commodity? A security? Or a new form of currency? The lack of clarity created a patchwork of regulations that still confuses users today.

In the United States, the Internal Revenue Service (IRS) took a hardline stance early on. In Notice 2014-21, the IRS declared that virtual currencies are treated as property for federal tax purposes. This decision had massive implications:

- Capital Gains Tax: Every time you trade Bitcoin for dollars, or even use Bitcoin to buy coffee, you trigger a taxable event. You must calculate the gain or loss based on the difference between your purchase price and the current value.

- No Currency Deductions: Because it’s not legal tender, you can’t deduct losses from trading crypto in the same way you might offset business expenses with currency fluctuations.

- Recordkeeping Burden: Unlike cash, where you just spend it, crypto users must track the cost basis of every single coin they acquire. This creates a significant administrative burden for everyday users.

Meanwhile, other agencies see it differently. The Office of the Comptroller of the Currency (OCC) issued Interpretive Letter 1179 in 2020, classifying certain cryptocurrencies as currency for banking purposes. This allows banks to provide custodial services for crypto, treating it like a foreign currency rather than a stock. This contradiction creates regulatory tension. You are taxed like a trader by the IRS but handled like a banker by the OCC.

Real-World Impact: Divorce, Death, and Disputes

The abstract debate over classification becomes very concrete when lives change. Consider estate planning. In traditional scenarios, physical jewelry is distributed immediately after death. Bank accounts, however, are often frozen for months during probate because they are intangible debts owed by the bank.

A 2023 report from the American Academy of Estate Planning Attorneys found that 42% of probate cases involving digital assets required judicial clarification of their classification. Compare that to just 7% for traditional assets. Families are stuck in limbo because judges aren't sure if Bitcoin should be treated like a stock (personal property) or cash (currency). If it's property, it goes through probate. If it's currency, it might pass directly to beneficiaries via beneficiary designations, similar to a retirement account.

Divorce cases face similar chaos. The American Academy of Matrimonial Lawyers reported in 2022 that 31% of high-net-worth divorces involved disputes over crypto classification. Should Bitcoin be split evenly as marital property? Or is it separate property if acquired before marriage? Courts across different states have given inconsistent rulings, leaving couples with unpredictable outcomes.

| Asset Type | Legal Classification (US) | Tax Treatment | Transfer Mechanism |

|---|---|---|---|

| Physical Cash | Tangible Personal Property / Medium of Exchange | No direct tax until spent/exchanged | Hand-to-hand delivery |

| Bank Account Balance | Intangible Personal Property (Chose in Action) | Interest income taxed as ordinary income | Electronic Fund Transfer Act (EFTA) rules |

| Bitcoin/Crypto | Property (IRS) / Virtual Asset (EU MiCA) | Capital Gains Tax on every transaction | Blockchain transfer / Private keys |

| Stablecoins | Contested (Often Property) | Capital Gains (if pegged asset fluctuates) | Smart contract execution |

Global Shifts: The EU Model and Future Frameworks

The United States is not alone in struggling with this. Globally, lawmakers are realizing that the binary choice between "property" and "currency" is obsolete. The European Union took a step forward with the Markets in Crypto-Assets (MiCA) regulation, which became effective in June 2024. MiCA classifies cryptocurrencies as "virtual assets," creating a distinct category separate from both traditional property and fiat currency. This approach acknowledges that crypto has characteristics of both but fits neatly into neither.

In the US, the Uniform Law Commission revised the Uniform Electronic Transactions Act in 2023 to address these gaps. By September 2023, 18 states had adopted provisions clarifying how digital assets are treated in contracts and estates. Meanwhile, the IRS released draft guidance in 2024 proposing a three-tier system:

- Tier 1: Government-issued currency (legal tender).

- Tier 2: Stablecoins pegged to fiat currency (treated closer to currency).

- Tier 3: Non-pegged cryptocurrencies like Bitcoin (treated as property).

This tiered approach aims to reduce the compliance burden for stablecoin users, who often use them for daily transactions similar to cash. However, until this is finalized into law, the old rules apply.

Practical Steps for Asset Owners

So, what should you do with this information? First, stop assuming your crypto behaves like cash. If you are using Bitcoin or Ethereum for daily purchases, you are likely underreporting capital gains. Use accounting software that tracks cost basis automatically. Tools like CoinTracker or Koinly integrate with wallets to generate tax reports, saving you from manual spreadsheets.

Second, review your estate plan. If you hold digital assets, ensure your will or trust explicitly addresses them. Specify whether they should be treated as divisible property or transferred via private key inheritance mechanisms. Consult an attorney familiar with the Uniform Law Commission’s model acts to ensure your wishes are legally binding in your state.

Finally, stay aware of jurisdictional differences. If you travel or do business internationally, remember that the EU treats crypto as a virtual asset, while Asia may view it as a commodity or prohibited item. Your legal protection depends entirely on where you are standing.

Is Bitcoin considered property or currency by the IRS?

As of 2026, the IRS continues to classify Bitcoin and most cryptocurrencies as property for tax purposes, following Notice 2014-21. This means you must pay capital gains tax on any increase in value when you sell, trade, or spend it. It is not treated as legal tender or currency for tax deductions.

How does the EU classify cryptocurrency compared to the US?

The European Union uses the MiCA regulation, which classifies crypto as "virtual assets," a distinct category from both traditional property and fiat currency. The US currently lacks a unified federal definition, leading to conflicting treatments where the IRS sees it as property and the OCC sometimes treats it as currency for banking compliance.

Do I have to pay taxes if I buy coffee with Bitcoin?

Yes. Because the IRS treats Bitcoin as property, spending it is a taxable event. You must calculate the fair market value of the Bitcoin at the time of the transaction and compare it to your original purchase price. If the value has increased, you owe capital gains tax on that profit, even if it's just a few cents.

What happens to my crypto if I die without a will?

Without a will, your crypto likely goes through probate as part of your estate. Since it is classified as property, it may be frozen or difficult to access until a court appoints an executor. This process can take months or years. To avoid this, include specific instructions for digital asset inheritance in your estate plan.

Are stablecoins treated differently than Bitcoin?

Currently, the IRS still treats most stablecoins as property, meaning they are subject to capital gains tax. However, proposed IRS guidance suggests a future tiered system where stablecoins pegged to fiat currency might receive treatment closer to currency, reducing the tax reporting burden for small transactions.

Mark Corpuz

June 6, 2026 AT 13:40The distinction between tangible and intangible property is fascinating, but it feels archaic when applied to digital assets. We need a legal framework that recognizes the fluid nature of blockchain technology rather than forcing it into 18th-century boxes.

Steven Jacobowitz

June 8, 2026 AT 10:52Wait, so if I use Bitcoin to buy coffee, I have to report capital gains? That seems insane for small transactions. The administrative burden alone would kill adoption. How do you even track cost basis for every single micro-transaction?

Sylvia Mossman

June 10, 2026 AT 08:04This whole system is rigged against the little guy. The IRS wants their cut, but they won't give us the tools to comply easily. It's just another way to punish people who try to opt out of the traditional banking system.

Alexis Abster

June 10, 2026 AT 18:15I was totally unaware of this! I thought crypto was just like digital cash. This changes everything for my estate planning. I need to talk to a lawyer immediately before it's too late.

Brad Ranks

June 11, 2026 AT 16:11Drama alert: My uncle died last year and his Bitcoin is still stuck in probate because nobody knew how to classify it. It’s been eight months and we can’t touch a dime. This isn’t theoretical, folks.

Lee Paige

June 12, 2026 AT 11:20The government is trying to control your money by making it illegal to use anything other than fiat. They call it 'tax compliance' but it's really about surveillance. If you don't want to be tracked, you're forced into the shadows.

Alexander DeVries

June 12, 2026 AT 23:04Let's look at the facts here. The EU's MiCA regulation is actually a step forward. By creating a distinct category for virtual assets, they are acknowledging reality instead of pretending Bitcoin is just a stock or a dollar bill.

Caralee Robertson

June 14, 2026 AT 07:56i read this and im so confused lol. does this mean i owe taxes on my doge coins? pls help

Greg Lewis

June 15, 2026 AT 09:13property is an illusion anyway. what you own is just a story agreed upon by society. crypto exposes the fragility of that story. when the narrative shifts so does the value. we are all just holding pieces of paper with numbers on them

JEVON HALL

June 15, 2026 AT 09:57Pro tip: Use CoinTracker or Koinly. They connect to your wallets and auto-calculate the cost basis. It saves hours of manual entry. Don't try to do this in Excel unless you enjoy pain 😅

Dr Lynea LaVoy

June 16, 2026 AT 11:01As an estate planning attorney, I can confirm that the lack of clarity is causing significant issues. Clients often assume their digital assets will pass smoothly, but without explicit instructions in their wills, families face legal hurdles. Please consult a professional.

dan kaffeman

June 17, 2026 AT 01:51You people are idiots if you think the government cares about your privacy. They want every transaction recorded. Crypto is only useful if you understand how to launder it properly, otherwise you're just feeding the beast.

Meg Gran

June 17, 2026 AT 16:47oh sure, let's pretend the irs has any interest in fairness. they just want more revenue. and now they get to tax air? yeah right. its a joke.

Caitlin Donahue

June 18, 2026 AT 20:57I think we should all just ignore the rules until they change. If everyone stops reporting, maybe they'll be forced to create a simpler system. Just my two cents though!

Karthikeyan S

June 19, 2026 AT 00:59the problem is that most users are uneducated. they buy meme coins and then cry when the tax man comes. its not the systems fault its their lack of financial literacy. stop whining and start learning 📉

Dinesh Pattigilli

June 19, 2026 AT 16:42Only the elite understand the true nature of these assets. The rest of you are just gambling with your life savings. The regulatory framework is designed to protect the sophisticated investors from the rabble.

Madhu Menon

June 21, 2026 AT 00:15It is interesting to see how ancient laws adapt to new technologies. Perhaps this is a sign that our understanding of ownership itself is evolving. What does it mean to own something that exists only as code?

Narendra Kulkarni

June 21, 2026 AT 17:02Thanks for sharing this info. I had no idea about the divorce implications either. Good thing my wife and I don't have much crypto yet, but good to know for the future.

verna kennedy

June 23, 2026 AT 00:39If you cannot manage your tax obligations, you do not deserve to participate in the market. It is that simple. Competence is required for freedom.

Kelly Tenney

June 24, 2026 AT 01:13Don't worry everyone, there are plenty of resources available to help. Let's support each other in navigating these complex rules. We can figure this out together!

Matthew Malone

June 25, 2026 AT 13:55Typical American inefficiency. Other countries have figured this out. We are stuck arguing over definitions while losing ground globally. Pathetic.

Mark Corpuz

June 26, 2026 AT 14:43I agree with the point about global competition. The US needs to modernize its approach quickly or risk becoming irrelevant in the digital economy.